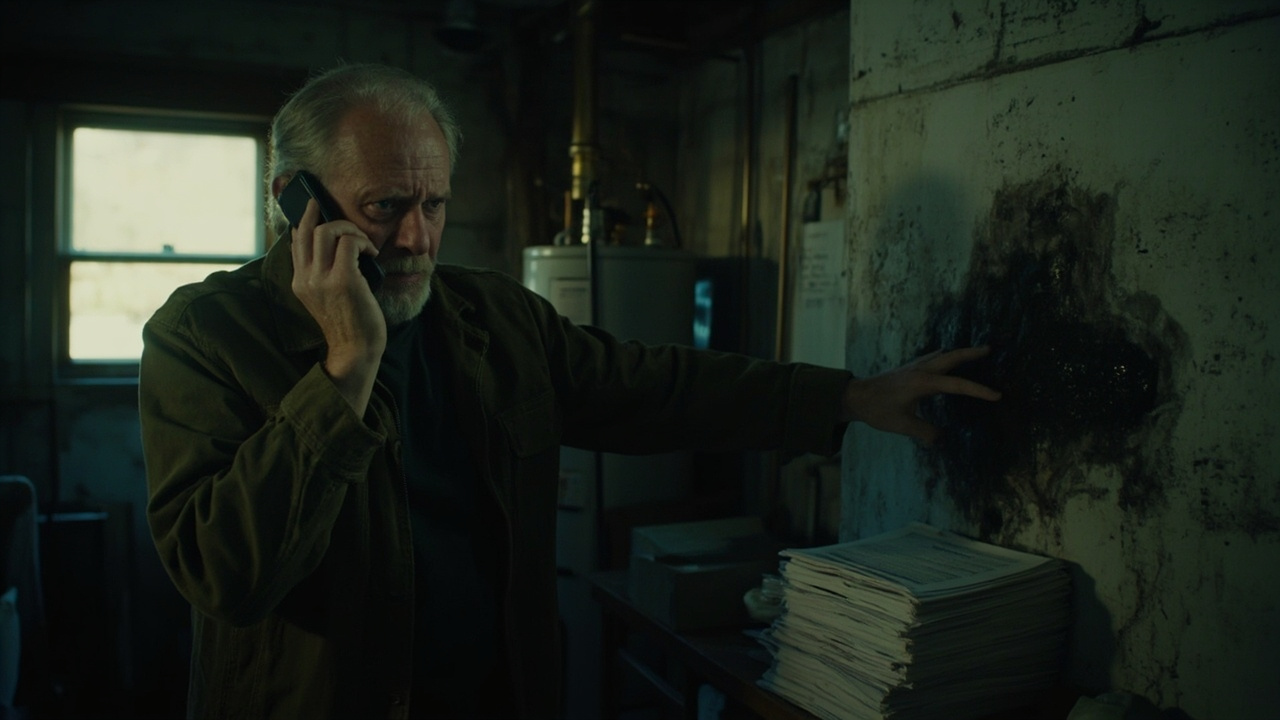

Seattle's proximity to Puget Sound creates consistently high humidity levels year-round, typically ranging between 70 and 85 percent. Most mold species thrive above 60 percent humidity. This constant moisture exposure means Seattle homes face elevated mold risk even without catastrophic water damage events. Insurance adjusters in this region scrutinize mold claims more carefully because they know mold can develop from ambient humidity rather than covered perils. You must prove the mold resulted from sudden water intrusion, not gradual moisture accumulation from normal Seattle weather patterns. Professional documentation showing moisture levels, spore types, and damage patterns becomes critical evidence separating covered claims from maintenance-related denials.

Washington State insurance regulations require specific disclosures about mold coverage limitations. Most homeowners policies now include mold exclusion endorsements that cap coverage between $5,000 and $15,000, regardless of actual remediation costs. Seattle homeowners purchasing older homes in neighborhoods like Fremont, Wallingford, or the University District should review their policies carefully, as these areas contain many pre-1950 homes with outdated moisture management systems. Local restoration companies understand these regional insurance nuances and can recommend supplemental mold coverage endorsements before problems occur. We also maintain relationships with public adjusters who specialize in contesting low settlement offers when insurers attempt to apply policy limitations unfairly.